Lithium-Ion Battery Recycling Industry Report 2025: Market Growth, Technology Innovations, and Strategic Opportunities Unveiled

- Executive Summary and Market Overview

- Key Market Drivers and Restraints

- Technology Trends and Innovations in Lithium-Ion Battery Recycling

- Competitive Landscape and Leading Players

- Market Size, Growth Forecasts, and CAGR Analysis (2025–2030)

- Regional Analysis: Key Markets and Emerging Hotspots

- Challenges, Risks, and Regulatory Landscape

- Opportunities and Strategic Recommendations

- Future Outlook: Disruptive Trends and Long-Term Projections

- Sources & References

Executive Summary and Market Overview

The global lithium-ion battery recycling market is poised for significant growth in 2025, driven by the rapid expansion of electric vehicles (EVs), consumer electronics, and energy storage systems. As the demand for lithium-ion batteries surges, so does the imperative to manage end-of-life batteries sustainably, both to mitigate environmental risks and to recover valuable materials such as lithium, cobalt, nickel, and manganese. Recycling not only addresses the environmental hazards associated with improper battery disposal but also helps alleviate supply chain pressures for critical raw materials.

According to MarketsandMarkets, the global lithium-ion battery recycling market is projected to reach USD 9.2 billion by 2025, growing at a compound annual growth rate (CAGR) of over 21% from 2020. This growth is underpinned by stringent government regulations on battery disposal, increasing awareness of resource conservation, and the economic benefits of material recovery. The Asia-Pacific region, led by China, Japan, and South Korea, dominates the market due to its robust battery manufacturing ecosystem and proactive recycling policies.

Key industry players such as Umicore, Retriev Technologies, and Li-Cycle are investing heavily in advanced recycling technologies, including hydrometallurgical and direct recycling processes, to improve recovery rates and reduce environmental impact. These innovations are crucial as the composition of lithium-ion batteries evolves, with newer chemistries requiring tailored recycling solutions.

In 2025, the market landscape is also shaped by policy initiatives such as the European Union’s Battery Regulation, which mandates higher collection and recycling targets, and the U.S. Department of Energy’s Battery Recycling Prize, which incentivizes innovation in the sector (European Commission; U.S. Department of Energy). These regulatory frameworks are expected to accelerate investment and capacity expansion across the value chain.

Overall, 2025 marks a pivotal year for lithium-ion battery recycling, with the market transitioning from nascent pilot projects to large-scale, commercially viable operations. The sector’s growth is integral to the circular economy ambitions of the clean energy transition, ensuring both environmental stewardship and resource security.

Key Market Drivers and Restraints

The lithium-ion battery recycling market in 2025 is shaped by a dynamic interplay of drivers and restraints, reflecting both the surging demand for battery-powered technologies and the challenges inherent in recycling processes.

Key Market Drivers

- Rising Electric Vehicle (EV) Adoption: The global shift toward electric mobility is a primary catalyst. With EV sales projected to reach 17 million units in 2025, the volume of end-of-life batteries is set to increase significantly, fueling demand for recycling solutions (International Energy Agency).

- Resource Security and Critical Material Recovery: Lithium, cobalt, and nickel are essential for battery manufacturing but are subject to supply risks and price volatility. Recycling offers a sustainable pathway to recover these critical materials, reducing dependence on primary mining and supporting circular economy goals (World Bank).

- Stringent Environmental Regulations: Governments in Europe, North America, and Asia-Pacific are implementing stricter regulations on battery disposal and extended producer responsibility (EPR), compelling manufacturers and consumers to adopt recycling practices (European Commission).

- Technological Advancements: Innovations in hydrometallurgical and direct recycling processes are improving recovery rates and reducing costs, making recycling more economically viable (U.S. Department of Energy).

Key Market Restraints

- High Operational Costs: The collection, transportation, and processing of spent batteries remain capital-intensive, especially for small-scale recyclers. Fluctuating prices of recovered materials can further impact profitability (International Energy Agency).

- Technical Complexity and Safety Risks: Lithium-ion batteries are prone to thermal runaway and fire hazards during handling and dismantling, necessitating specialized infrastructure and expertise (Organisation for Economic Co-operation and Development).

- Fragmented Collection Systems: Inconsistent collection and sorting infrastructure, particularly in emerging markets, limit the volume of batteries available for recycling and hinder economies of scale (United Nations Environment Programme).

- Regulatory Uncertainty: Evolving standards and lack of harmonization across regions can create compliance challenges for multinational recyclers and slow market development (EUROBAT).

Technology Trends and Innovations in Lithium-Ion Battery Recycling

Lithium-ion battery recycling is undergoing rapid technological transformation as the global demand for electric vehicles (EVs), consumer electronics, and energy storage systems accelerates. In 2025, the industry is witnessing a shift from traditional pyrometallurgical and hydrometallurgical processes toward more sustainable, efficient, and cost-effective recycling methods. These innovations are driven by the need to recover valuable materials such as lithium, cobalt, nickel, and manganese, while minimizing environmental impact and supporting a circular economy.

One of the most significant trends is the advancement of direct recycling, also known as cathode-to-cathode recycling. This process preserves the structure of cathode materials, enabling their direct reuse in new batteries and reducing the need for energy-intensive refining. Companies like Redwood Materials and Li-Cycle Holdings Corp. are pioneering closed-loop systems that maximize material recovery rates and minimize waste.

Automation and artificial intelligence (AI) are increasingly integrated into sorting, disassembly, and material separation stages. Automated robotic systems can safely and efficiently dismantle battery packs, while AI-driven analytics optimize process parameters for higher yield and purity. For example, Umicore is investing in smart recycling facilities that leverage digital technologies to enhance throughput and traceability.

Hydrometallurgical processes are also evolving, with new solvent extraction and selective leaching techniques that reduce chemical consumption and improve selectivity for critical metals. Research into bioleaching—using microorganisms to extract metals—is gaining traction as a low-energy, environmentally friendly alternative, with pilot projects underway in Europe and Asia (International Energy Agency).

- Decentralized recycling: Modular, mobile recycling units are being deployed to reduce transportation costs and emissions, making it feasible to process batteries closer to the point of collection.

- Second-life applications: Before recycling, batteries are increasingly assessed for potential reuse in less demanding applications, such as stationary energy storage, extending their lifecycle and reducing waste (BloombergNEF).

- Policy-driven innovation: Regulatory frameworks in the EU, US, and China are mandating higher recycling rates and eco-design, spurring investment in advanced recycling technologies (European Commission).

In summary, 2025 marks a pivotal year for lithium-ion battery recycling, with technology trends focused on efficiency, sustainability, and circularity, underpinned by digitalization and regulatory support.

Competitive Landscape and Leading Players

The competitive landscape of the lithium-ion battery recycling market in 2025 is characterized by rapid expansion, strategic partnerships, and significant investments from both established industry leaders and innovative startups. As the global demand for electric vehicles (EVs) and energy storage systems accelerates, the need for sustainable end-of-life battery management has intensified, driving competition among recyclers to secure supply contracts, develop advanced technologies, and scale operations.

Key players in the market include Umicore, Retriev Technologies, Li-Cycle Holdings Corp., Ecobat, and GEM Co., Ltd.. These companies have established robust collection networks and proprietary recycling processes, such as hydrometallurgical and pyrometallurgical methods, to recover valuable metals like lithium, cobalt, and nickel from spent batteries. For instance, Umicore has expanded its closed-loop recycling model, supplying recovered materials back to battery manufacturers, while Li-Cycle Holdings Corp. has scaled its spoke-and-hub technology across North America and Europe, enabling efficient material recovery and regional supply chain integration.

Emerging players such as Redwood Materials and Battery Resourcers (Ascend Elements) are disrupting the market with innovative direct recycling techniques and partnerships with automakers and electronics manufacturers. Redwood Materials, for example, has secured agreements with Panasonic and Ford Motor Company to recycle production scrap and end-of-life batteries, while Ascend Elements is building new facilities in the U.S. to meet surging domestic demand.

- Strategic alliances between recyclers and OEMs are becoming increasingly common, as seen in partnerships between Ecobat and Stellantis, and GEM Co., Ltd. with CATL.

- Asian companies, particularly in China, maintain a dominant position due to government mandates and integrated supply chains, with GEM Co., Ltd. and Brunp Recycling leading in capacity and technology.

- European and North American markets are witnessing increased investment in local recycling infrastructure, driven by regulatory pressures and the need for supply chain resilience.

Overall, the lithium-ion battery recycling sector in 2025 is marked by consolidation, technological innovation, and a race to secure feedstock, positioning leading players to capitalize on the exponential growth in battery waste and the circular economy.

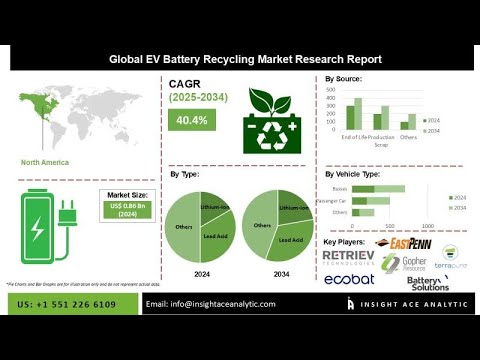

Market Size, Growth Forecasts, and CAGR Analysis (2025–2030)

The global lithium-ion battery recycling market is poised for significant expansion between 2025 and 2030, driven by surging demand for electric vehicles (EVs), energy storage systems, and stricter environmental regulations. According to MarketsandMarkets, the market size is projected to reach approximately USD 35.1 billion by 2030, up from an estimated USD 11.2 billion in 2025. This represents a robust compound annual growth rate (CAGR) of around 25.5% during the forecast period.

Several factors underpin this rapid growth trajectory. The exponential increase in EV adoption is generating a parallel surge in end-of-life batteries, necessitating efficient recycling solutions. Additionally, government policies in regions such as the European Union, China, and the United States are mandating higher recycling rates and the use of recycled materials in new batteries, further accelerating market expansion. For instance, the European Union’s Battery Regulation, effective from 2025, sets ambitious targets for lithium, cobalt, and nickel recovery, directly impacting recycling volumes and technology investments (European Commission).

Asia-Pacific is expected to dominate the market throughout the forecast period, with China leading both in battery production and recycling capacity. North America and Europe are also witnessing substantial investments in recycling infrastructure, with companies such as Umicore, Redwood Materials, and Li-Cycle expanding their operations to meet growing demand.

- Revenue Growth: The market is forecasted to add over USD 23 billion in new revenue between 2025 and 2030, reflecting both volume growth and higher value recovery from advanced recycling technologies.

- Volume Growth: The volume of spent lithium-ion batteries available for recycling is expected to increase at a CAGR of over 20%, as EVs purchased in the late 2010s and early 2020s reach end-of-life (BloombergNEF).

- Technology Trends: Hydrometallurgical and direct recycling methods are anticipated to gain market share due to their higher recovery rates and lower environmental impact compared to traditional pyrometallurgical processes.

In summary, the lithium-ion battery recycling market is set for dynamic growth from 2025 to 2030, underpinned by regulatory momentum, technological innovation, and the global shift toward electrification and circular economy principles.

Regional Analysis: Key Markets and Emerging Hotspots

The global lithium-ion battery recycling market is experiencing significant regional shifts as demand for electric vehicles (EVs), energy storage systems, and portable electronics accelerates. In 2025, key markets such as China, Europe, and North America are leading the charge, while emerging hotspots in Southeast Asia and Latin America are rapidly gaining traction.

China remains the dominant force, accounting for over 50% of the world’s lithium-ion battery recycling capacity. The country’s robust EV adoption, government-backed recycling mandates, and the presence of major players like GEM Co., Ltd. and BYD Company Ltd. have fostered a mature ecosystem. China’s “dual carbon” goals and extended producer responsibility (EPR) policies are expected to further boost recycling volumes in 2025, with the market projected to grow at a CAGR exceeding 20% through the decade (International Energy Agency).

Europe is emerging as a critical hub, driven by stringent EU regulations, such as the Battery Directive and the European Green Deal. Countries like Germany, France, and Sweden are investing heavily in recycling infrastructure, with companies such as Umicore and Northvolt expanding their operations. The region’s focus on circular economy principles and localizing battery supply chains is expected to result in a 30% increase in recycling capacity by 2025 (EUROBAT).

- North America is witnessing rapid growth, particularly in the United States and Canada. Federal incentives, state-level mandates, and investments from automakers like Tesla and General Motors are catalyzing the sector. Companies such as Redwood Materials and Li-Cycle are scaling up operations, with the U.S. Department of Energy supporting new recycling facilities (U.S. Department of Energy).

- Southeast Asia is an emerging hotspot, with countries like Indonesia, Malaysia, and Thailand investing in recycling to support their growing EV industries. Strategic partnerships and foreign direct investment are accelerating technology transfer and capacity building (Asian Development Bank).

- Latin America, particularly Brazil and Chile, is leveraging its role as a major lithium producer to develop domestic recycling capabilities, aiming to close the loop in the battery value chain (United Nations Economic Commission for Latin America and the Caribbean).

In summary, while China, Europe, and North America will continue to dominate the lithium-ion battery recycling landscape in 2025, emerging regions are poised to play increasingly important roles, driven by policy support, investment, and the global push for sustainable battery supply chains.

Challenges, Risks, and Regulatory Landscape

The lithium-ion battery recycling sector in 2025 faces a complex array of challenges, risks, and regulatory hurdles that shape its development and scalability. As demand for electric vehicles (EVs) and energy storage systems accelerates, the volume of end-of-life batteries is projected to surge, intensifying the need for efficient and sustainable recycling solutions. However, several critical issues persist.

One of the foremost challenges is the technical complexity of recycling lithium-ion batteries. These batteries contain a mix of valuable and hazardous materials, including lithium, cobalt, nickel, and manganese, often in varying chemistries and formats. Safe disassembly and material recovery require advanced processes to prevent fires, toxic emissions, and environmental contamination. The lack of standardized battery designs further complicates automated recycling and increases operational costs. According to International Energy Agency, the diversity in battery chemistries and form factors is a significant barrier to scaling recycling infrastructure.

Economic viability remains a persistent risk. The fluctuating prices of recovered materials, especially cobalt and nickel, can undermine the profitability of recycling operations. Additionally, the high capital expenditure required for state-of-the-art recycling facilities and the relatively low volume of end-of-life batteries (compared to future projections) can deter investment. McKinsey & Company notes that without policy incentives or stable material prices, many recycling ventures struggle to achieve commercial sustainability.

The regulatory landscape is rapidly evolving but remains fragmented across regions. In the European Union, the new Battery Regulation (effective 2025) mandates higher collection rates, stricter recycling efficiency targets, and minimum levels of recycled content in new batteries. This is expected to drive investment and innovation but also imposes compliance costs and reporting burdens on manufacturers and recyclers. In contrast, the United States lacks a unified federal framework, with regulations varying by state, creating uncertainty for market participants. European Parliament and U.S. Environmental Protection Agency highlight these regulatory disparities.

Finally, safety and environmental risks are paramount. Improper handling of lithium-ion batteries can result in fires, explosions, and toxic leaks, posing threats to workers and communities. Ensuring compliance with health, safety, and environmental standards is both a legal and reputational imperative for industry players.

Opportunities and Strategic Recommendations

The lithium-ion battery recycling market in 2025 presents a dynamic landscape shaped by surging electric vehicle (EV) adoption, tightening environmental regulations, and growing supply chain concerns for critical battery materials. These factors collectively create significant opportunities for stakeholders across the value chain, from recyclers and battery manufacturers to automotive OEMs and technology providers.

Opportunities:

- Supply Security for Critical Materials: As demand for lithium, cobalt, and nickel intensifies, recycling offers a strategic avenue to secure secondary sources of these materials. Companies that invest in advanced recycling technologies can reduce reliance on volatile primary markets and mitigate geopolitical risks. For instance, Umicore and Redwood Materials are expanding their recycling capacities to supply battery-grade materials directly to manufacturers.

- Regulatory Tailwinds: The European Union’s Battery Regulation, effective from 2025, mandates minimum recycled content in new batteries and strict collection targets, creating a robust market for compliant recycling solutions. Similar policy momentum is observed in the U.S. and Asia, incentivizing investment in recycling infrastructure (European Commission).

- Technological Innovation: Emerging direct recycling and hydrometallurgical processes promise higher recovery rates and lower environmental impact compared to traditional pyrometallurgy. Companies pioneering these methods, such as Li-Cycle, are well-positioned to capture market share as OEMs seek greener supply chains.

- OEM Partnerships and Vertical Integration: Automotive manufacturers are increasingly forming alliances with recyclers to ensure closed-loop supply chains. For example, Tesla and Volkswagen have announced initiatives to recycle end-of-life batteries from their EV fleets, reducing costs and enhancing sustainability credentials.

Strategic Recommendations:

- Invest in R&D: Stakeholders should prioritize research into next-generation recycling technologies that maximize material recovery and minimize environmental impact, positioning themselves for regulatory compliance and cost leadership.

- Expand Collection Networks: Building robust collection and reverse logistics systems will be critical to securing feedstock and meeting regulatory requirements, especially as EV battery volumes surge post-2025.

- Pursue Strategic Partnerships: Collaborations between recyclers, OEMs, and material suppliers can accelerate technology deployment, ensure steady material flows, and create competitive advantages.

- Monitor Policy Developments: Proactive engagement with policymakers and industry groups will help companies anticipate regulatory shifts and capitalize on emerging incentives or mandates.

In summary, 2025 will be a pivotal year for lithium-ion battery recycling, with significant opportunities for innovation, supply chain resilience, and regulatory-driven growth for proactive market participants.

Future Outlook: Disruptive Trends and Long-Term Projections

The future outlook for lithium-ion battery recycling in 2025 is shaped by a convergence of disruptive trends and long-term projections that are poised to redefine the industry landscape. As global demand for electric vehicles (EVs), consumer electronics, and renewable energy storage accelerates, the volume of end-of-life lithium-ion batteries is expected to surge, intensifying the need for efficient and sustainable recycling solutions.

One of the most significant disruptive trends is the rapid advancement of direct recycling technologies, which aim to recover cathode materials in their original chemical form, reducing the need for energy-intensive refining processes. Companies such as Redwood Materials and Li-Cycle Holdings Corp. are pioneering closed-loop systems that promise higher material recovery rates and lower environmental impact compared to traditional pyrometallurgical and hydrometallurgical methods.

Policy and regulatory frameworks are also evolving rapidly. The European Union’s proposed Battery Regulation, set to take effect in 2025, will mandate higher recycling efficiencies and minimum levels of recycled content in new batteries, compelling manufacturers and recyclers to innovate and scale up operations. Similar legislative momentum is building in the United States and Asia, with China already enforcing stringent recycling quotas for battery producers (European Commission; International Energy Agency).

Strategic partnerships between automakers, battery manufacturers, and recyclers are expected to proliferate, driven by the need to secure critical raw materials such as lithium, cobalt, and nickel. For instance, Tesla, Inc. and Panasonic Corporation have announced initiatives to integrate recycling into their battery supply chains, aiming to reduce reliance on volatile global mining markets and enhance supply chain resilience.

Looking ahead, market analysts project that the global lithium-ion battery recycling market could exceed $18 billion by 2030, with a compound annual growth rate (CAGR) of over 20% from 2025 onwards (MarketsandMarkets). This growth will be underpinned by technological innovation, regulatory pressure, and the economic imperative to recover valuable materials. However, challenges remain, including the need for standardized battery designs to facilitate recycling, investment in collection infrastructure, and the development of scalable, cost-effective recycling processes.

In summary, 2025 marks a pivotal year for lithium-ion battery recycling, with disruptive technologies, regulatory shifts, and strategic collaborations setting the stage for long-term industry transformation and sustainability.

Sources & References

- MarketsandMarkets

- Umicore

- Retriev Technologies

- Li-Cycle

- European Commission

- International Energy Agency

- World Bank

- United Nations Environment Programme

- Redwood Materials

- BloombergNEF

- Ecobat

- GEM Co., Ltd.

- Stellantis

- CATL

- BYD Company Ltd.

- Northvolt

- General Motors

- Asian Development Bank

- United Nations Economic Commission for Latin America and the Caribbean

- McKinsey & Company

- European Parliament

- Volkswagen